Webcast

(Using a version of the January Investor Deck)

19:10 We learned the passion for that in-ring content from our most passionate fans

First 22 minutes

* 2017 Financials

* Bragging about YouTube dominance & views

* Joseph Campbell’s Monomyth (“Everyone knows what happens in a ring.”)

* We put different content on different platforms.

* Half the broadband homes in the world have a WWE fan!

* Key Content Distribution Agreements expire in 2019

* Long-tail opportunity is 25% revenue/75% of video consumption comes int’l

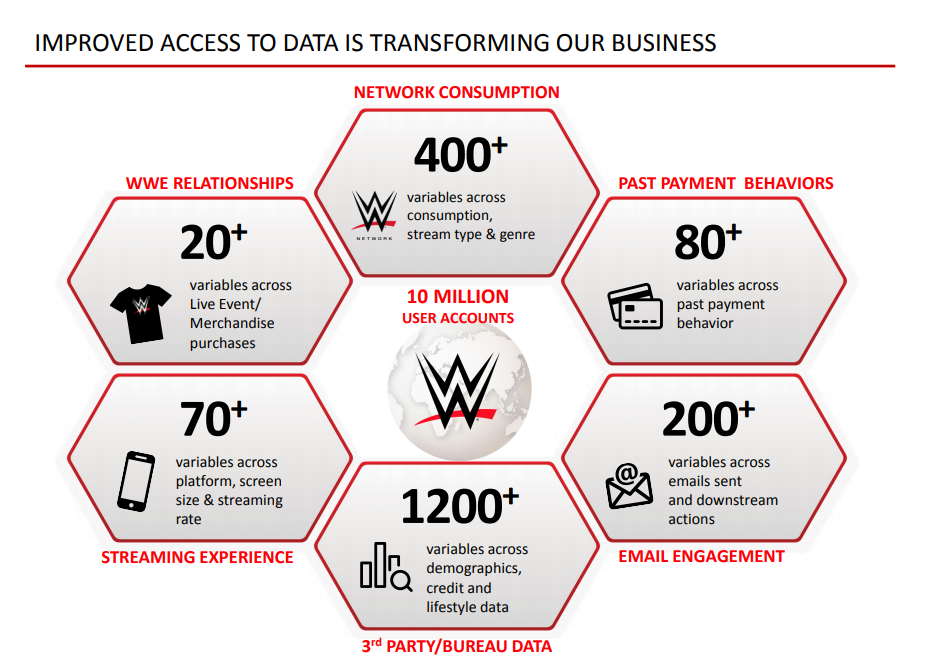

* We have over 10,000,000 user accounts across all our platforms

Investment Priorities

* Content

* Emerging Markets

* Technology

21:30 Q&A Begins

Q: Where are the current levels of the sports rights revenue in the US. Given the metrics you’ve put up and the popularity of the sport, it seems like it could be bigger.... What are the prospects for really accelerating and why haven’t we seen more of that in the past?

A: In 2014, our top seven deals generated about $130m. In, 2018 will generate about $235m. That’s a 80% increase over four years. By any metric, we’re one of the largest purveyors of live data in the world. In United States, our core content has under-monetized relative to others if you believe ratings are right metric. This next renewal cycle will answer that question about whether we’re able to narrow that gap.

24:00

Q: Could we see broadcasters actively interested in the rights or will it be predominately a cable property?

A: Distribution is more at risk than it’s ever has been for a network. Theoretically, it’s always been at risk, but practically speaking, today with skinny bundles… viewership is incredibly important. Our numbers are out there. They’re public. Everyone can see the scale of both the size of our audience and as well as how much time they spend consuming our content. So I’d like to think if on the other side, if you monetize from generating distribution revenue and ad revenue, we’d be an attractive property in that environment. We’ll announce something between May and September.

25:00

Q: Any thoughts on digital players coming in for some of those rights and actually competing for those rights? How would you think about licensing television rights to a digital player?

A: Are they active and in the market? Amazon has secured rights for live content, primarily Tennis in the UK. Everyone knows that Facebook did bid pretty aggressively for the digital rights of the IPL, which is Cricket in India.

For the last ten years, there’s been talk of the digital players actually becoming active participants in the live rights ecosystem which is more valuable but also more expensive. The last 12-18 months, those are no longer rumors - they’re active.

FaceBook launched the Watch tab, I’m not sure if we were the first call, second or third, but we were one of the first calls to create original live content for that platform. They’re trying to create a new viewing behavior. The watch tab is an active experience where you’re going to seek out video as compared to the lean-back experience of the news feed. They’re trying it first with YouTube. They called us. We did a great new show with them - Mixed Match Challenge. They’re seem to be happy. There’s not a lot of benchmarks to compare it against. Time per video spent - grew. What I think they’re trying to do - that’s what important to everyone. It continues to grow. The fourth quarter was the biggest quarter for consumption and video views and monetization on YouTube.

27:45

Q: As a rights holder how do you think about those platforms?

I think it’s a combination of reach, some cases the reach may not be where the traditional players are, in some cases it’s greater reach but it’s behavior - are people used to and willing to consume long-form video on that platform. If they make a pivot and they’re not, you can damage the overall brand.

Our view is “it will come”. People will watch long-form video on those platforms.

I think it’s a combination of reach, some cases the reach may not be where the traditional players are, in some cases it’s greater reach but it’s behavior - are people used to and willing to consume long-form video on that platform. If they make a pivot and they’re not, you can damage the overall brand.

Our view is “it will come”. People will watch long-form video on those platforms.

It’s not a matter of if, it’s a matter of when. The behavior is already changing.

We tested Raw & Smackdown viewership on YouTube - full episodes - in certain parts of the world - so we can see it. We did that because we wanted to see the behavior.

It’s kind of a march towards that. If you make that in this renewal cycle, you are making a bet that’s going there.

We tested Raw & Smackdown viewership on YouTube - full episodes - in certain parts of the world - so we can see it. We did that because we wanted to see the behavior.

It’s kind of a march towards that. If you make that in this renewal cycle, you are making a bet that’s going there.

Similar we thought six or seven years ago, we thought direct-to-consumer was going to grow and that would be the way to reach the consumer.

We’ll see how the world shakes out and what the future holds.

29:20

Q: I was looking at the over-the-top growth numbers you were putting out.

We’ll see how the world shakes out and what the future holds.

29:20

Q: I was looking at the over-the-top growth numbers you were putting out.

A: Over-the-top is so 2013.

Q: Direct to consumer, you’re about one and half million subs. Just looking at the numbers you put out. Looks like growth has slowed. Do you think there’s room to accelerate it? Why given the popularity of your content, why isn’t it actually growing faster? Some media company has over the top services that have more subscribers.

A: The thing to remember about is, what I mentioned with the tiering of the content.

The direct-to-consumer is not for every person out there. May not be for new WWE fan or even a casual WWE fan. They get a lot of that content already. They get Raw & Smackdown for 5 hours a week.We’ll produce 600 hours for the digital platform. So they get that content.

So really, the direct-to-consumer is for the portion of the fanbase who is super passionate.

Having said that, it’s four years in, we thought we could get it to three or four million subs. Four years in, we’re about half-way there, to the 3 million. So, we feel great. It’s the second largest business we have. Second most profitable.

It’s is the hub of the direct-to-consumer strategy. It’s where we engage. Where the most time is spent.

30:50

A: The thing to remember about is, what I mentioned with the tiering of the content.

The direct-to-consumer is not for every person out there. May not be for new WWE fan or even a casual WWE fan. They get a lot of that content already. They get Raw & Smackdown for 5 hours a week.We’ll produce 600 hours for the digital platform. So they get that content.

So really, the direct-to-consumer is for the portion of the fanbase who is super passionate.

Having said that, it’s four years in, we thought we could get it to three or four million subs. Four years in, we’re about half-way there, to the 3 million. So, we feel great. It’s the second largest business we have. Second most profitable.

It’s is the hub of the direct-to-consumer strategy. It’s where we engage. Where the most time is spent.

30:50

I think to re-accelerate the growth, part of it would be localization. Today is a US product.

25% of our subscribers come from outside the US. It’s $9.99 so that price point doesn’t work everywhere. It’s only in US currency. So you’re asking a potential fan in some markets to take the FX risk. Sounds wonky but it’s actually an issue. People realize that. That they’re taking that in certain markets. It’s only in English.

It’s designed a US product that because of the ubiquity of broadband we’ve made available.

I think that localizing would help bend that curve.

We think there’s an opportunity to tier that product.

On the higher end of the tier, it’s an ARPU-play (average revenue per user).

On the lower end, integrating free video, like you see today on WWE.com with the premium video - there’s an opportunity for both to improve conversion and retention. So that’s what we’re working on.

In the short and intermediate term, because what I just described is in essence a new product, in the short & intermediate term, it’s using the data to drive better and better retention and acquisition. That’s what we’re hard at work on.

32:05

25% of our subscribers come from outside the US. It’s $9.99 so that price point doesn’t work everywhere. It’s only in US currency. So you’re asking a potential fan in some markets to take the FX risk. Sounds wonky but it’s actually an issue. People realize that. That they’re taking that in certain markets. It’s only in English.

It’s designed a US product that because of the ubiquity of broadband we’ve made available.

I think that localizing would help bend that curve.

We think there’s an opportunity to tier that product.

On the higher end of the tier, it’s an ARPU-play (average revenue per user).

On the lower end, integrating free video, like you see today on WWE.com with the premium video - there’s an opportunity for both to improve conversion and retention. So that’s what we’re working on.

In the short and intermediate term, because what I just described is in essence a new product, in the short & intermediate term, it’s using the data to drive better and better retention and acquisition. That’s what we’re hard at work on.

32:05

Q: Does it make sense to maybe try to move some of the content you have on other digital platforms into the direct-to-consumer. It’s always a balancing act. What Netflix has shown us is you’ve have to make some make some investment and take some pain for awhile, but if you make the content exclusive and the and it’s a rich place for the source of content, you’ll grow subs but it’s hard to have your cake and eat it too. How do you think about that balancing out?

A: Yeah, it is. We call it the “delicate balance” internally because when we’re creating those 1,500 hours of content the real question is “What platform to put it on?”. Obviously we think we’re tiering it correctly today, because it’s what we’re doing. but it’s something I think overall, over time... The simplest way to think about it is we can drive significant sub growth tomorrow by putting Raw or SmackDown on the Network. It may not be the right thing to do, either for the brand or for short-term monetization. That’s an extreme case but to frame the question. Those are the decisions we have to make every day.

We don’t think it’s about more content on the direct-to-consumer, right now. There’s a lot of content on there today. As a reminder, it’s is different from CBS All Access which is essentially CBS in another form. This is unique content for our most passionate fans. It’s not for all 160 million broadband homes in the world. It’s for a fairly small percentage of those homes where people really really want to go deep. We think the content strategy is right. We don’t think is more necessary more. It’s some of the other things I mentioned: Functionality, Features, some of the tiering I mentioned is a bigger opportunity.

34:00

Q: Someone in the company said, yeah we’re open to, when asked about being a public company, do you want to comment on that?

A: If you’re referring to .. in 2016…

Q: Whatever.. Can you comment on that approach?

A: Yeah, it is. We call it the “delicate balance” internally because when we’re creating those 1,500 hours of content the real question is “What platform to put it on?”. Obviously we think we’re tiering it correctly today, because it’s what we’re doing. but it’s something I think overall, over time... The simplest way to think about it is we can drive significant sub growth tomorrow by putting Raw or SmackDown on the Network. It may not be the right thing to do, either for the brand or for short-term monetization. That’s an extreme case but to frame the question. Those are the decisions we have to make every day.

We don’t think it’s about more content on the direct-to-consumer, right now. There’s a lot of content on there today. As a reminder, it’s is different from CBS All Access which is essentially CBS in another form. This is unique content for our most passionate fans. It’s not for all 160 million broadband homes in the world. It’s for a fairly small percentage of those homes where people really really want to go deep. We think the content strategy is right. We don’t think is more necessary more. It’s some of the other things I mentioned: Functionality, Features, some of the tiering I mentioned is a bigger opportunity.

34:00

Q: Someone in the company said, yeah we’re open to, when asked about being a public company, do you want to comment on that?

A: If you’re referring to .. in 2016…

Q: Whatever.. Can you comment on that approach?

A: I’ll go back to the quote, Vince gave when given the context of all of the media consolidations, someone asked him, would you consider something like that.

His answer was “We’re open for business. We’re creative people in both storytelling as well as business. All we care about is entertaining our fans and doing that in the best way possible. We are always looking at creative ideas.”

His answer was “We’re open for business. We’re creative people in both storytelling as well as business. All we care about is entertaining our fans and doing that in the best way possible. We are always looking at creative ideas.”

12 comments:

A GREAT SPELL CASTER (DR. EMU) THAT HELP ME BRING BACK MY EX GIRLFRIEND.

Am so happy to testify about a great spell caster that helped me when all hope was lost for me to unite with my ex-girlfriend that I love so much. I had a girlfriend that love me so much but something terrible happen to our relationship one afternoon when her friend that was always trying to get to me was trying to force me to make love to her just because she was been jealous of her friend that i was dating and on the scene my girlfriend just walk in and she thought we had something special doing together, i tried to explain things to her that her friend always do this whenever she is not with me and i always refuse her but i never told her because i did not want the both of them to be enemies to each other but she never believed me. She broke up with me and I tried times without numbers to make her believe me but she never believed me until one day i heard about the DR. EMU and I emailed him and he replied to me so kindly and helped me get back my lovely relationship that was already gone for two months.

Email him at: Emutemple@gmail.com

Call or Whats-app him: +2347012841542

Thanks for sharing this informative article. I will check out your blog regularly for the latest posts. I will check out your blog regularly for some updated posts. The information in this article is related to the topic Instagram fake dm. This information can be used to check real and fake Instagram Direct Messages.

The style is so unique. Thanks for publishing this kind of blog, Keep blogging!... MM

Excellent site you’ve got here. I appreciate individuals like you! Take care!!... MM

Lot of interesting information here. Thank you for sharing. keep it up... MM

Thanks for a very interesting blog. Waiting for the next blog updates... MM

Its full of information here that I am looking for, Great work you have in here!... MM

I am so blessed to discover this. thank you

This is very interesting, I love how you express yourself in form of writing.

You’re a very skilled blogger. thank you

Good blog you have got here.. It’s hard to find quality writing like yours these days.

Thank you for sharing.

Post a Comment